All Categories

Featured

Table of Contents

For those ready to take a bit much more threat, variable annuities provide extra possibilities to grow your retirement possessions and potentially increase your retirement earnings. Variable annuities provide a series of investment alternatives managed by professional money supervisors. Because of this, capitalists have extra adaptability, and can even relocate assets from one alternative to an additional without paying taxes on any type of financial investment gains.

* An instant annuity will certainly not have a buildup phase. Variable annuities issued by Safety Life Insurance Company (PLICO) Nashville, TN, in all states except New York and in New York City by Safety Life & Annuity Insurer (PLAIC), Birmingham, AL. Stocks supplied by Investment Distributors, Inc. (IDI). IDI is the principal underwriter for signed up insurance items released by PLICO and PLAICO, its affiliates.

Capitalists need to thoroughly take into consideration the financial investment purposes, dangers, charges and costs of a variable annuity and the underlying investment choices prior to spending. This and other information is included in the programs for a variable annuity and its underlying investment options. Prospectuses might be acquired by calling PLICO at 800.265.1545. An indexed annuity is not a financial investment in an index, is not a safety or securities market financial investment and does not participate in any stock or equity investments.

What's the distinction between life insurance coverage and annuities? The bottom line: life insurance coverage can help offer your enjoyed ones with the monetary tranquility of mind they are worthy of if you were to pass away.

What is an Variable Annuities?

Both ought to be considered as component of a long-term financial strategy. Although both share some similarities, the general purpose of each is really different. Let's take a fast look. When comparing life insurance policy and annuities, the largest distinction is that life insurance policy is designed to assist protect against an economic loss for others after your death.

If you wish to learn even more life insurance policy, checked out the specifics of exactly how life insurance coverage functions. Consider an annuity as a tool that might aid meet your retirement demands. The key purpose of annuities is to develop earnings for you, and this can be carried out in a couple of various ways.

How does an Annuities help with retirement planning?

There are numerous possible advantages of annuities. Some include: The ability to expand account worth on a tax-deferred basis The capacity for a future income stream that can't be outlived The possibility of a lump sum advantage that can be paid to a surviving partner You can buy an annuity by offering your insurer either a solitary lump amount or paying over time.

Individuals normally acquire annuities to have a retired life earnings or to build savings for another objective. You can buy an annuity from an accredited life insurance representative, insurer, economic planner, or broker. You ought to speak with a monetary adviser concerning your needs and objectives before you acquire an annuity.

What is the best way to compare Annuities For Retirement Planning plans?

The distinction between the two is when annuity settlements start. allow you to save cash for retirement or various other factors. You do not have to pay tax obligations on your profits, or payments if your annuity is an individual retired life account (INDIVIDUAL RETIREMENT ACCOUNT), till you withdraw the profits. allow you to produce an earnings stream.

Deferred and prompt annuities supply numerous choices you can pick from. The options offer different levels of prospective threat and return: are guaranteed to make a minimal rate of interest. They are the lowest monetary danger but supply reduced returns. make a higher rate of interest price, but there isn't a guaranteed minimum interest rate.

allow you to select in between sub accounts that resemble mutual funds. You can earn more, but there isn't an ensured return. Variable annuities are greater threat due to the fact that there's a chance you might shed some or every one of your money. Set annuities aren't as high-risk as variable annuities because the investment danger is with the insurer, not you.

If efficiency is low, the insurance provider births the loss. Set annuities assure a minimal rate of interest, normally between 1% and 3%. The firm might pay a higher rate of interest than the guaranteed rates of interest. The insurer figures out the rates of interest, which can change regular monthly, quarterly, semiannually, or yearly.

What does a basic Annuity Investment plan include?

Index-linked annuities show gains or losses based on returns in indexes. Index-linked annuities are extra complex than fixed postponed annuities (Fixed vs variable annuities).

Each depends on the index term, which is when the company computes the interest and credit scores it to your annuity. The identifies how much of the increase in the index will be made use of to compute the index-linked interest. Various other crucial functions of indexed annuities consist of: Some annuities top the index-linked rate of interest.

Not all annuities have a flooring. All dealt with annuities have a minimal surefire value.

What are the tax implications of an Secure Annuities?

The index-linked passion is contributed to your initial premium quantity however doesn't compound throughout the term. Various other annuities pay compound passion throughout a term. Compound passion is rate of interest gained on the money you saved and the rate of interest you gain. This indicates that rate of interest already attributed likewise makes rate of interest. In either case, the passion gained in one term is generally worsened in the next.

If you take out all your money before the end of the term, some annuities will not attribute the index-linked interest. Some annuities might attribute only component of the passion.

How can an Deferred Annuities protect my retirement?

This is due to the fact that you bear the financial investment risk as opposed to the insurance firm. Your representative or monetary advisor can help you determine whether a variable annuity is ideal for you. The Securities and Exchange Commission classifies variable annuities as safeties since the efficiency is stemmed from supplies, bonds, and other financial investments.

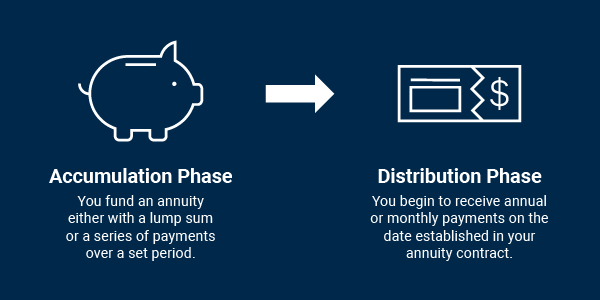

Discover more: Retirement ahead? Believe about your insurance coverage. An annuity agreement has two phases: an accumulation phase and a payout stage. Your annuity earns interest throughout the accumulation stage. You have a number of options on how you contribute to an annuity, depending on the annuity you purchase: allow you to pick the time and amount of the payment.

{kind=link}

Table of Contents

Latest Posts

Analyzing Strategic Retirement Planning Everything You Need to Know About Financial Strategies Breaking Down the Basics of Investment Plans Features of Smart Investment Choices Why Choosing the Right

Exploring Fixed Vs Variable Annuity Pros And Cons Key Insights on Indexed Annuity Vs Fixed Annuity Defining the Right Financial Strategy Pros and Cons of Variable Vs Fixed Annuities Why Choosing the R

Highlighting the Key Features of Long-Term Investments A Comprehensive Guide to Investment Choices Breaking Down the Basics of Fixed Index Annuity Vs Variable Annuity Benefits of Choosing the Right Fi

More

Latest Posts